The crypto stock rollercoaster just delivered another twist. On February 25, 2026, Circle Internet Group (NYSE: CRCL) shares exploded 35%+ in a single session—the biggest one-day pop since its IPO—after crushing Q4 2025 earnings. Revenue hit $770 million (up 77% YoY), USDC circulation reached $75.3 billion (up 72%), and on-chain transaction volume smashed records at $11.9 trillion (up 247%). Yet the stock still sits roughly 70% below its June 2025 all-time high of ~$299.

This isn’t just another earnings beat. It’s the comeback story of a company that went from Wall Street’s most oversubscribed IPO to a brutal 75-80% drawdown, only to rebound on pure fundamentals. Welcome to Circle’s rocky road to redemption—and why crypto investors should be paying attention.

Circle Internet Group, Inc. Class A Trade Ideas — NYSE:CRCL — TradingView

The Historical Timeline: From 2013 Payments Startup to Public Stablecoin Powerhouse

Circle didn’t start as a stablecoin giant. Founded in 2013 as a peer-to-peer payments company, it pivoted hard in 2018 with the launch of USDC alongside Coinbase—positioning itself as the transparent, regulated alternative to Tether’s USDT.

The road to public markets was bumpy:

- 2021-2022: SPAC deal valued at $9 billion collapses amid crypto winter and regulatory heat.

- 2023: SVB collapse triggers a brief USDC depeg to $0.87. Circle recovers fast with full reserves and transparency reports—building investor trust that still pays dividends.

- June 5, 2025: IPO at $31/share. Demand is insane (25x oversubscribed). Shares pop to $95 on day one, then rocket to $263-299 by June 23 as stablecoin hype peaks.

- Mid-2025 to early 2026: Federal Reserve rate cuts hammer interest income. Crypto market cools. CRCL crashes 70-80% to lows near $50. Short sellers pile in.

Then came Q4 2025 earnings. The market finally woke up to what Circle had been building quietly: real utility, not just yield.

Circle beats Q4 earnings estimates as USDC supply jumps 72%, shares surge 20% — TradingView News

Earnings Breakdown: Step-by-Step Mechanics of the Surge

Let’s unpack the numbers like a blockchain transaction—transparent and verifiable:

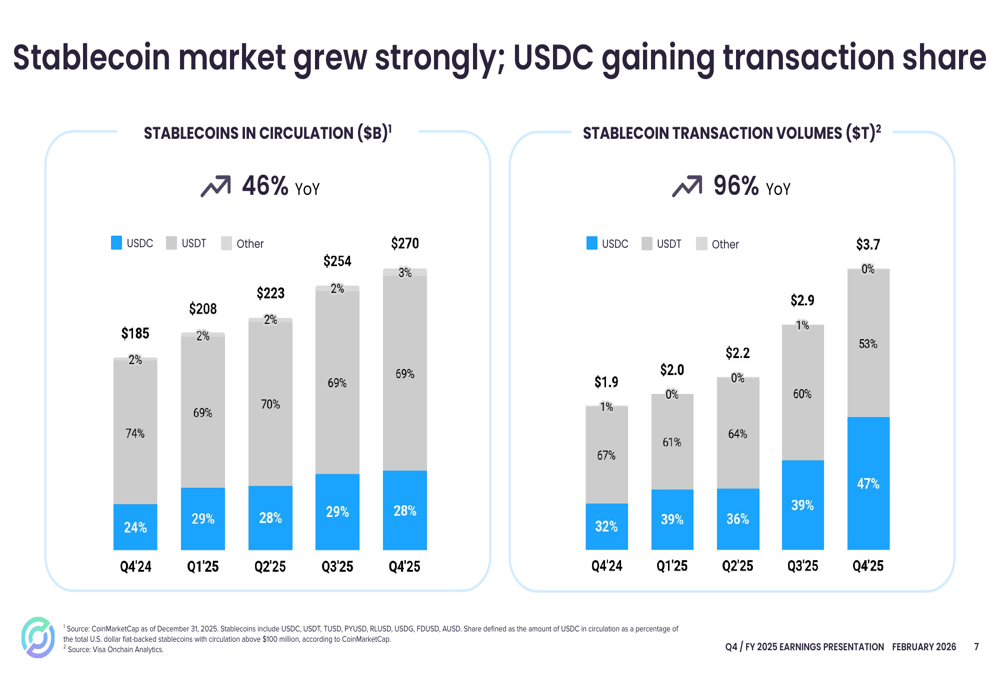

- USDC Growth Engine — Circulation hit $75.3B at year-end (+72% YoY, beating the company’s own 40% CAGR guidance). Average balances doubled. This isn’t retail FOMO; it’s institutions and enterprises using USDC for treasury, trading, and payments.

- Revenue Explosion — Q4 total revenue + reserve income = $770M (+77% YoY, beating estimates). Reserve income alone: $733M (+69%), even as the reserve return rate dipped to 3.8% from rate cuts. Volume more than made up for it.

- Transaction Velocity — On-chain USDC volume: $11.9T in Q4 (+247% YoY). That’s not just trading pairs—it’s real settlement. USDC now captures ~47% of all stablecoin transaction volume (up from 32% a year ago).

- Profitability Flip — Q4 net income: $133M. Adjusted EBITDA: $167M (+412%). Full-year 2025 showed a $70M net loss only because of $424M in one-time IPO-related stock-based compensation. Strip that out, and adjusted EBITDA hit $582M (+104%).

- Margin Magic — Revenue Less Distribution Costs (RLDC) margin expanded to 40%—above guidance. Operating leverage is kicking in hard as the business scales.

The market’s verdict? CRCL closed February 25 at ~$83, traded as high as $90 intraday, and continues showing strength around $84 as of February 27.

Circle Q4 2025 slides: USDC growth doubles guidance, margins surge, By Investing.com

Real-World Impacts: Where USDC Is Actually Moving Money

Circle isn’t just printing digital dollars—it’s embedding them into the real economy:

- Visa & JPMorgan Partnerships: USDC now powers instant settlements and cross-border rails. Visa’s latest initiatives and JPMorgan’s multiple USDC pilots show traditional finance finally adopting.

- Enterprise Integrations: Businesses are using Circle’s programmable wallets and payout tools for global payroll and supplier payments—cheaper and faster than SWIFT.

- Global Adoption Hotspots: Emerging markets (think high-inflation regions) and crypto-native platforms are driving velocity. USDC’s share of stablecoin volume is rising even as total stablecoin market cap grows.

- Arc Testnet Momentum: Circle’s Layer-1 blockchain (public testnet with 100+ participants) is already handling millions of daily transactions with sub-second finality—setting up the next leg of growth.

This is the shift from “yield farming” to “utility farming.” And the market is starting to price it in.

Risks and Short Interest: The Volatility That Won’t Quit

No redemption story is complete without the scars:

- Interest Rate Sensitivity — Reserve income still dominates. More Fed cuts could pressure margins (though non-interest revenue guidance of $150-170M for 2026 helps diversify).

- Competition — Tether still holds ~60% market share. Circle’s edge is regulation and transparency, but USDT’s liquidity is sticky.

- Short Squeeze Dynamics — High short interest fueled part of the February surge. Expect continued volatility.

- Regulatory Tailwinds (and Headwinds) — Pro-crypto U.S. policy (SAB 121 repeal talk, stablecoin legislation) is bullish, but execution matters.

Circle remains a high-beta play—great for believers, nerve-wracking for the faint-hearted.

Future Outlook: 2026 Guidance and the Path to Profitability

Management is doubling down:

- USDC circulation: 40% CAGR medium-term target.

- 2026 non-interest revenue: $150-170M.

- RLDC margins: 38-40%.

- Adjusted operating expenses: $570-585M.

If USDC hits these growth targets and Circle’s diversification (payments network, tokenized assets, Arc mainnet) scales, analysts see a clear path to sustainable profitability. Some price targets already sit at $130+.

The stock is still down massively from highs, but trading at ~2x 2025 revenue with real growth accelerating. That’s the redemption arc crypto investors love.

The Bottom Line: Redemption Complete?

Circle’s 2026 surge isn’t hype—it’s fundamentals catching up to the narrative. From SPAC failure to IPO pop to brutal drawdown to earnings-driven rebound, the company has proven it can weather crypto winters and rate storms.

For investors, the lesson is clear: Bet on utility, not just yield. USDC isn’t just surviving—it’s thriving as the regulated digital dollar.

What do you think— is CRCL a buy on this dip, or are we still early in the comeback?

Stay ahead of the next crypto stock move—subscribe to Cryptopress.site for deep dives, earnings breakdowns, and on-chain alpha delivered straight to your inbox.