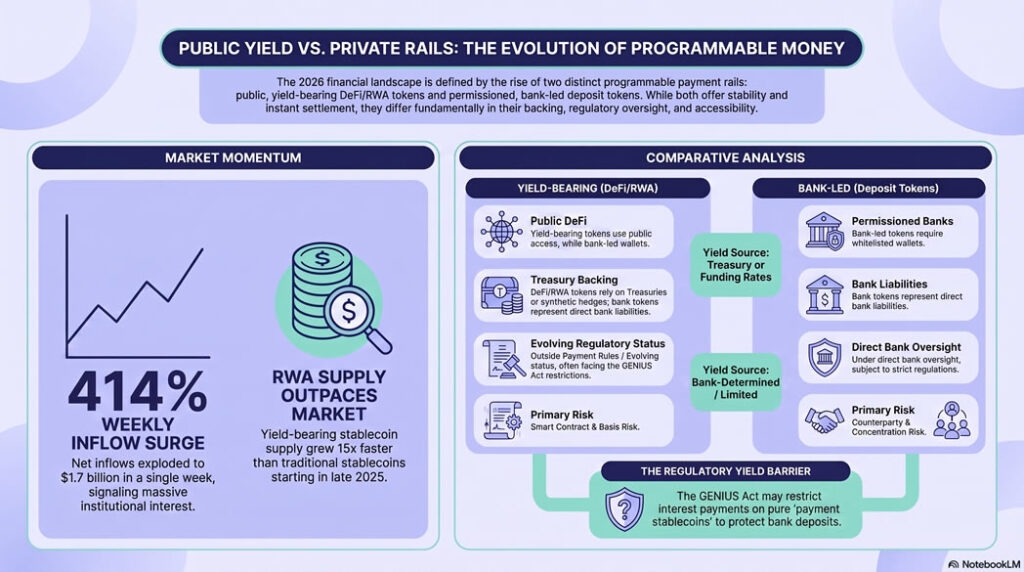

A $1.7 Billion Signal in One Week

Last week, while Washington continued wrestling with how — or whether — digital dollars should generate yield, stablecoin markets delivered a concrete verdict. Net inflows exploded 414% to $1.7 billion, according to Messari data, a report from Alexander Beaudry and Austin Freimuth. This wasn’t scattered retail speculation. It reflected institutions and sophisticated users actively allocating capital into instruments that combine the stability of dollars (or gold) with the ability to earn returns and move value instantly across programmable rails.

This surge captures the central tension and opportunity of 2026: the simultaneous rise of yield-bearing stablecoins (mostly public, DeFi- or RWA-native) and bank-led tokenized deposits (permissioned, compliance-first). Both are reshaping how value is stored, transferred, and monetized — yet they operate under very different regulatory and technical logics.

Think of traditional stablecoins as a checking account that pays 0% interest. Yield-bearing versions are closer to a high-yield savings account or Treasury bill fund — but fully liquid, transferable 24/7, and composable with other on-chain applications.

What Are Yield-Bearing Stablecoins?

Traditional stablecoins like USDT and USDC function as digital cash: 1:1 backed, redeemable, but earning zero yield while sitting idle. Yield-bearing versions change the equation.

They fall into two broad categories:

- RWA-backed (Real-World Asset): The stablecoin represents a claim on interest-bearing assets such as U.S. Treasuries or money market funds. Ondo’s USDY or similar tokenized treasury products pass through the yield from short-term government securities. Circle’s USYC and Paxos’ USDG variants have shown explosive growth in this segment.

- Synthetic / DeFi-native: Ethena’s USDe (and staked sUSDe) is the clearest example. Users mint USDe by depositing collateral; the protocol runs a delta-neutral strategy (long spot or equivalent, short perpetual futures). The funding rate paid by leveraged traders becomes the yield source — often in double digits during favorable conditions, though variable and subject to basis risk. sUSDe has at times captured tens of billions in supply by offering competitive returns with dollar stability.

Growth context: Yield-bearing stablecoin supply outpaced the broader stablecoin market by more than 15x starting in mid-October 2025. Specific names posted eye-popping gains: USYC +198%, USDG +169%, with others like USDY and USDD also climbing sharply. Projections suggested the category could exceed $50 billion in 2026 before some DeFi-native products saw pullbacks in Q2 amid yield compression and macro shifts.

Think of traditional stablecoins as a checking account that pays 0% interest. Yield-bearing versions are closer to a high-yield savings account or Treasury bill fund — but fully liquid, transferable 24/7, and composable with other on-chain applications.

Bank-Led Stablecoins and Permissioned Rails: JPMorgan’s Kinexys Play

Parallel to public yield products, traditional banks are building their own on-chain rails — not to compete on retail yield, but to modernize wholesale payments and tokenization.

JPMorgan’s Kinexys (formerly Onyx) is the most advanced example. It is a permissioned blockchain platform for programmable payments, asset tokenization, and near-real-time settlement. Key components include:

- JPM Coin (JPMD): A 1:1 USD deposit token issued on Coinbase’s Base (Ethereum L2) and expanding to other networks like the privacy-focused Canton Network. Institutional clients use whitelisted wallets to transfer value, post collateral, or settle transactions instantly on public infrastructure while remaining within JPM’s compliance perimeter.

- Blockchain Deposit Accounts (BDAs): Tokenized bank deposits now supporting eight currencies (USD, EUR, GBP + five APAC currencies added in 2026: AUD, HKD, JPY, RMB, SGD). This enables 24/7 FX and settlement far beyond traditional banking hours.

- Kinexys Fund Flow: A solution that records investor register and transactional data on-chain, already live with J.P. Morgan Private Bank, Asset Management, and Citco.

JPMorgan reports Kinexys has processed over $4 trillion in volume. The bank explicitly positions private/permissioned blockchains as potentially more impactful for traditional finance than public-chain narratives like MicroStrategy’s Bitcoin holdings.

Key difference from public stablecoins: Bank-led tokens represent direct bank liabilities, benefit from existing regulatory oversight and deposit insurance frameworks (in some structures), and prioritize compliance and interoperability with legacy systems. They sacrifice open permissionlessness for speed, finality, and regulatory comfort.

The Regulatory Crucible: GENIUS Act, OCC Approvals, and the Yield Question

The U.S. finally moved toward comprehensive stablecoin legislation with the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act in 2025. The OCC has emerged as the primary implementer.

Under proposed rules (March 2026):

- Permitted Payment Stablecoin Issuers (PPSIs) can be subsidiaries of national banks, uninsured national trust banks, non-bank entities, or foreign branches meeting thresholds.

- Strict 1:1 reserve requirements in high-quality liquid assets, capital and liquidity rules, regular reporting (weekly/quarterly), and robust AML/KYC.

- Critical restriction: Many proposals prohibit or severely limit the payment of interest or yield directly on “payment stablecoins” to avoid disintermediating bank deposits.

Approvals in motion:

- Coinbase received conditional OCC approval for a national trust bank charter.

- Paxos and Circle have pursued or received pathways.

- Sony Bank (via Connectia Trust) secured conditional approval for a U.S. national trust subsidiary focused on dollar stablecoins (targeting 2027 operations).

The yield debate is fierce. Pro-innovation voices argue that banning yield on stablecoins stifles competition and forces capital into less regulated wrappers. Bank advocates and some researchers warn that interest-bearing stablecoins could trigger significant deposit outflows and contraction in bank lending — with one analysis estimating potential lending reductions in the hundreds of billions to over $1 trillion under certain scenarios.

This regulatory friction explains why many yield products operate as DeFi or RWA wrappers rather than pure “payment stablecoins” under the new framework.

On-Chain Reality Check: PAXG Wallet Activity and Profit-Taking

Public data from Santiment provides a real-time pulse. In early July 2026, PAX Gold (PAXG) — Paxos’ physically backed, on-chain gold token — recorded an all-time high in daily active addresses (8,830) alongside realized profits hitting a 5-month peak of roughly $6.77 million.

This is instructive. Even as some yield-bearing products saw supply contraction in Q2, tokenized real-world assets like PAXG demonstrated robust wallet engagement and profit-taking behavior during gold’s broader rally. Holders are actively using on-chain gold exposure — not just for speculation, but as a practical store-of-value and liquidity tool. Exchange outflows and new wallet creation alongside profit realization suggest a maturing, rotating participant base rather than pure hype.

PAXG’s activity serves as a proxy for broader interest in on-chain RWAs that can complement or substitute for yield strategies in uncertain macro environments.

Real-World Applications and Economic Impact

- Treasury & Corporate Cash Management: Multinationals and funds can now park dollars in yield-bearing stables or tokenized bank deposits earning competitive returns while retaining instant transferability and 24/7 liquidity.

- Cross-Border Payments & FX: Kinexys-style rails and public stablecoins drastically reduce settlement times (from days to seconds/minutes) and costs compared with traditional correspondent banking.

- DeFi Composability: Yield-bearing stables integrate directly into lending, derivatives, and structured products.

- Emerging Markets & Inflation Hedging: In high-inflation jurisdictions, these instruments (especially gold-backed or USD yield products) offer practical alternatives to local currency depreciation. On-chain accessibility lowers barriers versus traditional offshore accounts.

Comparison Table:

| Feature | Traditional Stablecoins | Yield-Bearing (DeFi/RWA) | Bank-Led Deposit Tokens (e.g. JPM Coin) |

|---|---|---|---|

| Primary Backing | Cash / T-bills | RWAs or synthetic hedges | Bank deposits / reserves |

| Yield | None | Variable (Treasury or funding rates) | Limited / bank-determined |

| Permission Model | Public | Public | Permissioned (whitelisted) |

| Regulatory Status | Evolving (GENIUS) | Often outside pure payment stablecoin rules | Direct bank oversight |

| Best For | Payments, liquidity | Treasury yield, DeFi | Institutional settlement, tokenization |

| Key Risk | Depeg / reserve opacity | Smart contract / basis risk | Counterparty (bank) + concentration |

Challenges and Risks

Regulatory uncertainty remains the largest overhang. Final GENIUS rules on yield, capital, and foreign issuer treatment will determine whether growth accelerates or fragments into parallel systems.

Economic disintermediation: Research consistently shows that scalable interest-bearing alternatives can pull deposits from banks, potentially affecting lending capacity.

Operational & Market Risks: DeFi yield products carry smart-contract and strategy risks (funding rate flips). Bank tokens concentrate risk in the issuing institution. Both face run risk in stress scenarios, though transparent reserves and regulatory oversight mitigate (but do not eliminate) this.

Yield Compression: As more capital enters, attractive yields may normalize downward, reducing the “pull” factor observed in 2025.

Future Outlook

The second half of 2026 and beyond will likely see:

- More OCC national trust bank charters and PPSI approvals.

- Multichain expansion of bank tokens (JPM already signaling moves beyond Base).

- Hybrid models where public yield wrappers and permissioned bank rails interoperate.

- Tokenization of broader asset classes accelerating on both public and private infrastructure.

- Stablecoin supply potentially approaching or exceeding $400+ billion as utility deepens.

The 414% inflow week was not an anomaly — it was a preview of capital’s directional preference when yield, speed, and regulatory progress align.

Conclusion: From Speculative Asset to Financial Infrastructure

Yield-bearing stablecoins and bank-led tokenized deposits are no longer niche experiments. They represent a structural upgrade to how money works: always-on, programmable, and increasingly capable of generating returns without sacrificing stability or compliance.

For institutions, the opportunity lies in treasury efficiency and new settlement rails. For individuals — especially in environments where local currencies lose value quickly — these tools offer practical options for preserving and growing purchasing power on-chain.

The regulatory path is still being paved, but the direction is clear: programmable money is moving from the margins into the core of global finance.

Ready to go deeper? Subscribe to Cryptopress.site for ongoing analysis of stablecoin mechanics, RWA tokenization, regulatory developments, and on-chain data stories. Explore our related evergreen guides on DeFi yields, cross-border payments, and the economics of digital assets. DYOR, understand the risks, and position thoughtfully as this infrastructure matures.

Data and developments current as of mid-2026. Markets and regulations evolve rapidly — always verify latest figures and rules.